Tightening, War, and Innovation

May we live in interesting times

After over a decade of near-zero and ever-falling interest rates, nonexistent inflation, and a stock market that, by and large, only ever outdoes itself, we’re now in very different times. Inflation is high, the Fed is tightening - oh, and there’s a land war in Europe. For a generation of investors, including myself, these are uncharted waters. And by “investor”, I mean anyone who makes decisions about allocating capital - startup founders included.

The set of questions we have to ask ourselves is: What will happen, on what time horizon, and how should I allocate my capital to achieve my goals?

As I try to answer these questions for myself, I think there’s a realistic scenario in which this short-term business cycle and risk-off environment resolve themselves before start-up valuations, on the whole, are affected very much. That’s not to say every start-up is going to get through this macro environment; many start-ups fail even in good times, and some will now fail or face down-rounds due to the unfortunate timing of their fundraising needs. But I’m still investing, and I’m still bullish that not only are there great companies to invest in, but that investing in and building great companies is actually the most important factor in the longer term for keeping inflation in check and building consumer wealth.

What will happen?

Investing in any environment requires understanding the different forces at work, and balancing their impact on an asset. For example, stock prices are hurt by tightening, inflation, and war, but helped by high consumer demand and technological innovation. Commodities are helped by inflation, war (uncertainty + sanctions), and high consumer demand, but hurt by tightening.

At the most basic level, we have a strong economy, high inflation, and a tightening central bank, with the added factors of long-term technological innovation and a geopolitical conflict:

Consumer demand has been high because people have been given a lot of money with Covid stimulus checks, have seen the nominal value of their assets increase due to quantitative easing, and have been able to borrow very cheaply due to persistent low interest rates - all of which leads them to buy more stuff. See my post from early 2021 for more on this.

Inflation is caused by an increase in the amount of money and credit relative to the supply of stuff (goods and services). As money and credit has increased, Covid- and war-related disruptions have limited the availability of stuff. The war is driving up energy prices, most obviously, but impacts a variety of other commodities and products as well.

The Fed’s goals are to balance inflation and growth. With inflation high and growth strong, it has moved to tighten. Higher interest rates will negatively impact stocks, real estate, venture capital - and while some of that is already priced in to assets, there is likely more normalization that will happen.

Uncertainty around geopolitical conflicts is typically bad for risk assets. Historically, though, the uncertain period leading up to war is bad for assets, but once war breaks out with certainty, assets actually tend to do well (Source: Swiss Finance Institute, 2015).

Technological innovation is good for stocks in the long term. Additionally, if Russia steps up its cyber tactics as one way to hurt the West, the demand for cybersecurity products and services may go up and be a strong area of the economy.

But these forces all interact with one another, making the overall impact hard to predict:

Consumer purchasing behavior can increase during inflationary periods, as people expect inflation to continue and therefore their cash to be worth less so they buy real goods. This contributes to further inflation.

Tightening decreases the amount of borrowing and spending in the economy, reining in inflation while also putting a damper on growth. But tightening because of a strong economy often results in an increase in asset prices, as investors become bullish when the Fed telegraphs that they think the economy is strong and resilient to tightening.

Technological innovation also reins in inflation as the cost of producing things decreases with automation and is nearly zero with software, though again, this is a long-term effect.

On what time horizon?

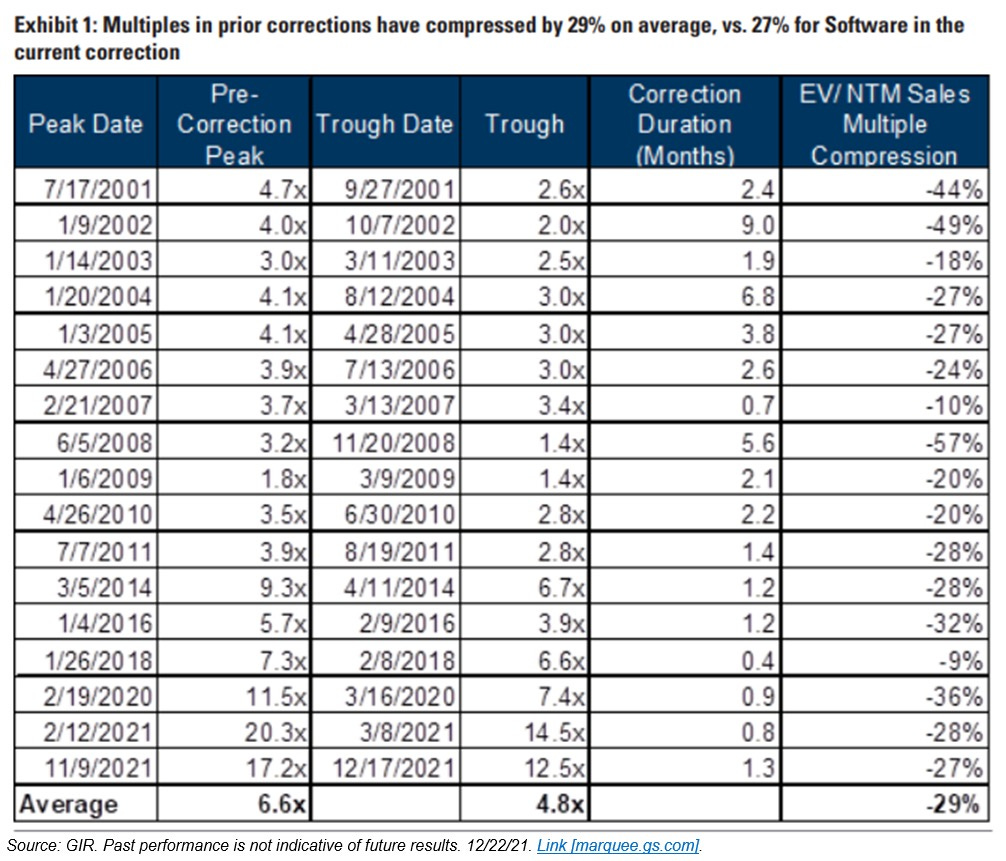

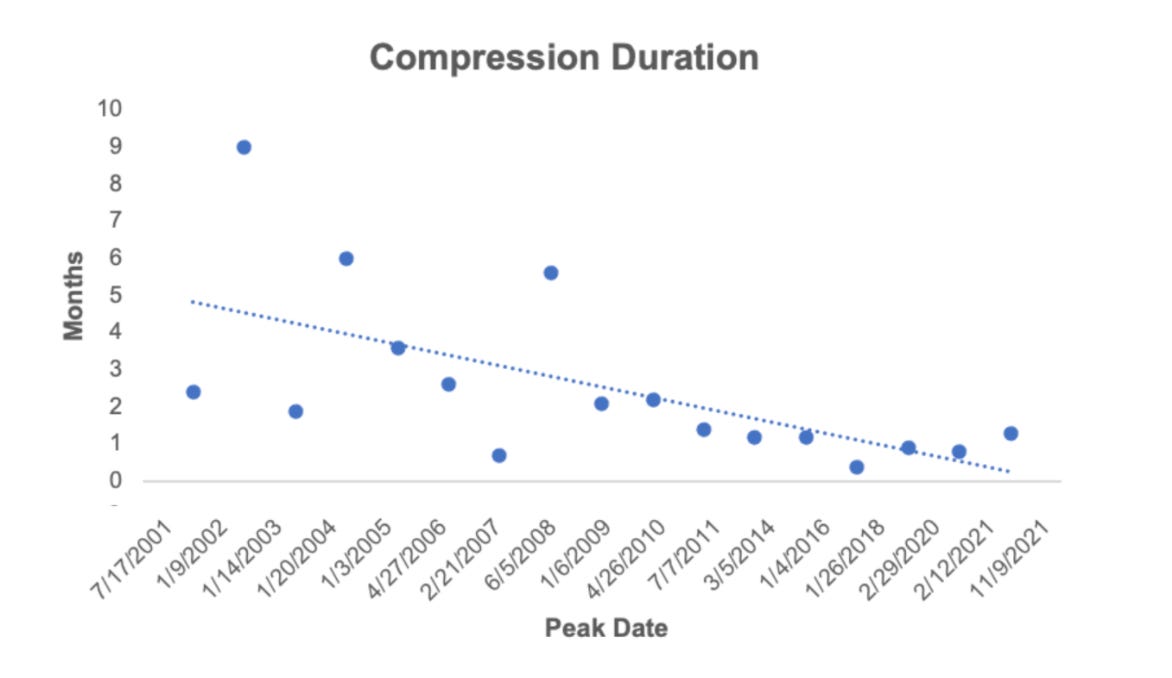

My friend Colin Denman recently pointed out that the duration of downturns in equity pricing has, broadly speaking, decreased over time. He sent me this table:

From which I created this chart:

This doesn’t include data on the current compression, as we’re still in the middle of it.

At the same time, the sizes of funding rounds have increased significantly these last few years - roughly in the range of 3.5x, across the board, from 2015 to 2021. Startups are, on the whole, extremely well-capitalized at the current moment. (Ideally I would have cash balances, but I don’t, so I’m using funding rounds as a proxy.)

Shorter compressions and bigger startup war chests are the two broad themes, and imply that the tech startup world might be able to get through this downturn relatively unscathed, even with likely further dips in the stock market. Of course, there’s a lot going on that could change this picture; investors tend to rely too much on the recent past to predict the future. We could end up in a low growth and high inflation environment, which is much slower and harder to get out of; Putin’s war could go a number of different ways that would probably be bad for risk assets.

And the flip side is, with big funding rounds came big valuations, so any pull-back in spending and growth to buy more time to wait out this downturn may come at the expense of reaching the lofty expectations that startups have raised on. Public market valuations may also have a real-time impact on startups who have public customers if demand from those customers decreases as a result of budget cuts.

How should I allocate capital?

Where I come out on all of this is that we’re in a relatively normal short-term business cycle and that the Fed will take the appropriate steps to curb inflation, and stop tightening if growth takes too much of a hit; the initial uncertainty of war has passed; and technological innovation is more important than ever. I’m still looking for businesses that are tackling a real problem, who are leaders in or creating a category - we’re long-term investors.

If I were a startup looking at a runway of >6 months, I would probably keep my existing growth plan and rate of burn on the expectation that the downturn will be over by the time I need to raise again. If I were a startup looking at a runway of less than 6 months, though, I’d either try to cut down and see how much time I can buy myself, understanding that I may not, as a result, get the valuation I’d been hoping for, or try to go out and fundraise now, understanding that the macro environment at this moment may also mean I don’t get the valuation I was hoping for.

Thanks to Colin Denman for inspiring this post and Sai Sriramagiri for support.